So you’ve sorted out your payment flows, and you’re wondering: how are they going to trip me up next?

Having delivered what we think is some pretty good news on this awful issue over the weekend, we’d be remiss not to try to bring you back down just a little with some more gory detail on how much else you’ll need to cover off before you can start feeling safe from an SRO or the ATO.

There’s been a private determination in one of the east coast states in the last few weeks which reinforces quite a bit the idea that fixing money flow is just part of a holistic equation.

You’ll also have to consider carefully the idea of “second supply”, or: is there anything else that your practice does which might make it look like your tenant doctor is providing services to the practice, not only to patients? Only to patients, is what it should look like (remember what the ATO says about employee vs contractor relationships: you have to look at the “entirety” of a business to work it out).

The first depressing thing about this determination is that this SRO didn’t use payment flows much in making its finding (although we suspect strongly that if it did, it would have found incorrect flows).

Here’s some of the things this SRO used to hang this practice for over $3m in back payroll tax (eight years’ worth!):

- It talked to (surveyed at the least) each of the tenant doctors without informing the practice and used that information to help assess the relationship. We don’t know, but we suspect they didn’t make the interviews or surveys feel entirely optional.

- It noted that the practice:

- Listed the so called tenant doctors on its website as “our doctors”

- Advertised directly to patients for services on behalf of doctors working at the practice, nor did the practice make any effort to explain that each doctor was offering their own services as a separate business

- Did not anywhere advertise its services to doctors as a service provider

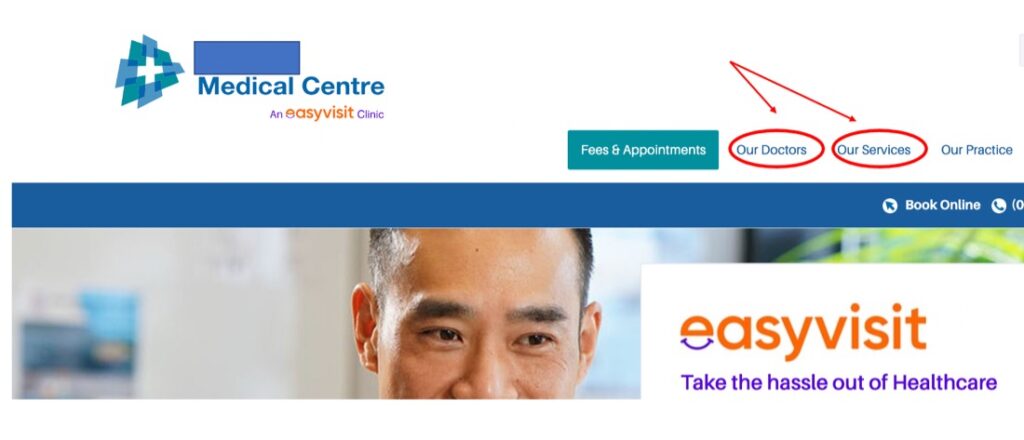

- Note: if you go to a big corporate site these days (eg, IPN), that’s pretty much all the corporate site does. Not withstanding, even with a group like IPN, when you get down to practice level, sometimes some of the mistakes listed here are still being made. Below is an IPN practice website, advertising ‘our doctors’, and pretty much doing most of what the SRO in this case saw as evidence of an employee/employer relationship (ie, no evidence of doctors advertising independently, central booking, et al)

- It noted that the tenant doctors did not anywhere make any attempt to market themselves directly to patient or present themselves as independent business. While not specifically saying it, this SRO was using tax law established federally that suggests anyone holding themselves out to be a business usually has a website. None of the tenant doctors had their own website! Imagine what this finding might end up meaning for tenant doctors across the country.

- That a “Google Streetview search” proved that the practice signage was exclusively promoting the practice and not promoting the individual services of the separate businesses of each tenanted doctor (Same for the practice above).

- The lease agreement had wording that included subletting restraints indicative of the tenants not actually being tenants

- The service agreements of tenant doctors:

- Had restraint clauses (a big no-no revealed in Thomas and Naaz)

- Were directive in how the tenant doctors operated, which was not in keeping with them being independent businesses

- The doctors had agreed conditions which allowed the clinics to issue RCTIs (recipient created tax invoices) for the services provided by the doctors to the clinics (RCTIs are apparently indicative of an employer arrangement not a tenant arrangement)

- Tenant doctor bookings were controlled by the practice entirely, either through the practice phone, or one of the booking engines

- The practice enforced “questionable and opaque” workplace policies and instructions via a workplace manual that indicated an employee arrangement not a contractor one

There are a lot more small moving parts in this case and others you are probably going to need to check and tick off for piece of mind, after payment flows are sorted.

We will be providing as much of this detail as we can in a webinar on August 9 that looks at everything we and several other experts have collected and seen that needs to be addressed in order to show you truly are just a form of medical AirBnB providing space and services for doctors.

One other clarification. Until now we have maintained that one of the intractable issue for practices was that you could not process payment flows easily because the rule was one ABN, one PRODA account. This view is reinforced by this paragraph in a story from the RACGP news service newsGP a few weeks ago:

“Where independent contractor doctors work at a practice, each doctor should have their own PRODA account and issue invoices with their own ABN (not the practice’s). If the doctor uses the practice’s PRODA account, that doctor may not be viewed as an independent contractor.”

We thought that this would prevent a PMS and practice processing their tenant doctor claims, suggesting it would need each tenant doctor’s PRODA to do it. We now think that is wrong.

Why?

Because in essence PRODA has nothing to do with actual dollar flows and processing payments. It is the replacement authentication system of a provider to PKIs (you’ll have to look that one up on Google, girls, I’ve got no space left to explain) brought in via the new web services arrangements of Services Australia.

You can use a single PRODA account for authenticating all your tenant doctor providers in a single PMS. The RACGP is still right in asserting a tenant doctor should issue invoices on their own ABN, and while individual doctors don’t need to worry about practices authenticating them, most will actually practically need their own PRODA account now for various other things, but first and foremost for setting up payments directly to their own account, one on one with Medicare. This can’t be done by a practice. But a tenant doctor PRODA account is not required to have a tenant doctor paid directly by Medicare once a tenant doctor is registered with their own ID via their own PRODA.

I bet that’s confused you. It’s fairly confusing. One thing that’s really confusing for practice owners and tenant doctors is the ideal workflow for establishing the correct payment flows if you want a tenant/landlord relationship. HW052 and HW027 are confusing still. You can bypass them now using your PRODA, but that process is not well understood still by most practices and doctors.

Probably Services Australia could step in with some ready reckoners here. Part of the issue we suspect in them not doing that is that they don’t want to start involving themselves in advising on tax issues, as they are not an SRO or an ATO.

It’s bit late, however, to be worrying about that. Services Australia needs to recognise that it has a mass of confused customers out there and part of that confusion has been driven by them moving to a web services set up and forcing every doctor to re-register for PRODA.

In a few weeks we will hold a detailed webinar which we hope will provide an up-to-date guide on everything in law and process that practices and tenant doctors can do to stay compliant on tax. You can register here for our Sorting out Payroll Tax and Income Tax Deep Dive webinar No 2, to be held on Tuesday 9 August at 7.30pm. The webinar will feature specialist accounting firm principal David Dahm, lawyer knowledgeable on gory detail, Lukasz Wyszynski, and CTO of Tyro, one of the key fintech providers in the middle of all this, Peter Williams.

If you missed Deep Dive 1, you can catch up here.